The UK Payments Council is currently carrying out a series of workshops around the UK, talking to clubs, charities and societies about the future of cheques. Communique, the Council’s new newsletter, says that these are to explore the organisation’s needs and the alternative to cheques. As far as I can see, though, cheques are already more of a pain than the alternatives. My wife recently had to collect a number of cheques from people in connection with a charity and it was a total hassle: it would have been so much easier if people had just PayPal’d the money to her. Keeping track of the cheques, one of which got lost in a pile of paperwork on my desk, and then depositing them, took time and effort that e-mail doesn’t. I couldn’t care less if I never see another cheque again, but the general public will need some time to get used to this. By way of example, a chap on Finextra asked:

Should the Payment Council have the right to change the method by which I bought my last car or might want to buy a conservatory in the future? Ford wouldn’t take the whole purchase on Credit card.

[From Details | LinkedIn]

Ford is not obliged to take cards at all, that’s got nothing to do with the Payments Council, it’s a matter of private contract. Ford could require you pay in cowrie shells or gold bars if they wanted to.

What if my Debit card had gone faulty or the phone connection had failed on the swipey box?

[From Details | LinkedIn]

What if your cheque book went soggy in the washing machine? What if you are illiterate?

Should the government make it a prerequisite to have a chequeing facility for a bank to be a bank?

[From Details | LinkedIn]

Interesting last point. The answer is no, of course, because bank regulation shouldn’t be anything to with payments. And payments regulation shouldn’t be anything to do with banks. Ever since the Payments Council announced its plan to end cheque clearing in 2018, there have been demands to keep them, and not just from charities, dentists, pressure groups representing the elderly, MPs and various other conservative groups.

The Federation of Small Businesses said it will ‘strongly oppose’ any move to get rid of cheques.

[From End of the cheque book: Traditional paper payment could be abolished by 2018 | Mail Online]

Fine. Let them pay for them then. Remember, it is not cheques that are being abolished in 2018 but cheque clearing. If your bank wants to offer you a cheque service, that is up to them. It will cost a fair bit more than debit cards, funds transfer or any other new-fangled payment mechanism though, because it involves messing around with bits of paper. If you are happy to pay for that, knock yourself out, I don’t have problem with that. But I don’t want to pay for you to do it, if you see what I mean. If some enterprising payments entrepreneur wants to set up a new cheque-clearing system that is paid for by its users, I’m all for competition. But the truth is that they could never make it work.

The price of a first class stamp for a standard letter will rise by 5p to 46p, while second class will go up by 4p to 36p. The rise for larger letters, such as some Christmas and birthday cards, is even more, with first class going up 9p to 75p.

[From Royal Mail: First class stamps to cost an extra 5p in record price rise | Mail Online]

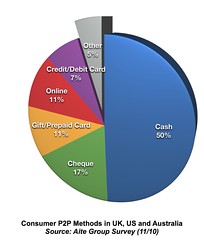

I can’t even post a cheque for less than P2P transaction would cost me, so why on earth people want to keep them I’ve no idea. As it is, they are only used for 11% of such transactions and there are plenty of alternatives available.

So nearly two-thirds of P2P transactions are still cash and cheques. What a fantastic opportunity for the e-payments industry and what a massive potential cost-saving for society. And this isn’t some hopeful projection: we already know that moving from cash and cheques to card leads to substantial savings.

The London Borough of Havering has appointed Citi to supply pre-paid cards to replace cash and cheque payments.

[From Finextra: London council halves cash processing costs by moving to pre-paid cards]

Potential uses for the pre-paid cards include, payments for social care budgets, asylum benefits, and housing benefits. Havering Council says the move will enable it to more than halve its existing processing costs for cash and cheque payments.

This seems reasonable: cards cost half of cash and cheques. Hopefully, come 2018, there will be a substantial fall in overall cost of payments to society. Who knows what the exact system, or systems, that replace cheques will be, but I think that we can already see that some combination of mobile, TV, cards and so on will do it. There are plenty of other countries where there are no cheques already and society doesn’t seem to have collapsed, so we can do the same.

This very morning I got a letter from my dentist reminding me to pay an outstanding invoice for £100 and asking me to send a cheque. As I could not be bothered to go and find the cheque book, write it out, put it in an envelope, address it and find a stamp., I thought I was just do by bank transfer next time I’m online. Oddly, the payment request did not either give bank account details or a PayPal address, so i sent them a message to ask. It turns out that they can take credit cards (with a 2.5% surcharge), debit cards and cheques only. Oh well. Since I had to log on this morning to pay a couple of bills, they would have had their money via FPS by now. As it is, I’ll pay with a cheque when I pop in for a check up in a few days time.

Dave, I think your assertion about cheques costing more than funds transfers is a bit sweeping… OK, if I transfer funds electronically between accounts with the same bank, it’s cheap and (usually) quick – but can also take as long as a cheque sometimes, for no apparent reason. And heaven help you if you want to transfer funds internationally or between currencies: in my experience that costs a great deal more than a cheque payment.

I agree that electronic payments are more convenient and even more secure than cheques, but I will be sad to see them go until the de-facto level of consumer protection is comparable.

We have several people per week contact us because they have been refused a refund for a fraudulent electronic transaction (card payment, online transfer, ATM withdrawal). I have never had someone contact us about being not refunded for a fraudulent cheque payment.

The lower usage level of cheques can partially explain this, but I don’t think fully. I can’t be sure though since the UK Cards Association (and as far as I know even the member banks) don’t collect statistics on denial of refunds.

When it comes to a fraudulent cheque transfer, the response “that isn’t my signature” seems to work well. When it comes to electronic transfers, the refusals are hard to argue with, e.g.:

“You understand that you are financially responsible for all uses of RBS Secure” (terms and conditions for online payments with RBS).

“Chip and PIN charges cannot be disputed as the card would have been in possession when charges were put through” (letter from American Express, concerning a Chip & PIN transaction)

“According to our records, all successful transactions were authorised with the genuine card and correct PIN” (letter from Halifax, concerning a Chip and PIN transaction).

Some customers are lucky and get their money back. For example in the last case merchant records showed that the Halifax’s records were wrong, tampered with, or misinterpreted and it was actually Chip & Signature transaction (with a forged signature). Or in the Emma Woolf case the police caught the bank employee which committed the fraud (probably by issuing herself a duplicate card), and so Abbey dropped the claim that it was Emma’s card and hence probably her fiancee who was defrauding her. Many customers aren’t as lucky through.

One of the best ways to remedy your ailing bank account is to get fast cash for gold. That means to sell gold and sell diamonds, and even watches and antiques. The global economic downfall has elicited a lot of mishaps to people’s finances.

i think if digital signatures are used instead of physical Signature then this problem can be solved .Although initially it was felt that there are high security measures are needed in this but in todays technically developed environment its no more an issue